Browse All Articles

The UK State of Spend: Who's Winning or Losing in H1 2026

Four signals from a shifting wallet — and what they mean for advertisers.

UK consumer spending looks healthy on the surface. Look closer, and the wallet is quietly diverging.

New analysis from Cardlytics, drawing on UK purchase data across more than 60 million enabled accounts, shows positive year-on-year spend growth across every macro category in H1 2026. But transactions, customer counts, and basket sizes tell a very different story underneath.

Consumers are protecting holidays, paying more for fewer nights out, and trading down on the high street.

Three shifts leaders shouldn't ignore

Holidays held, but restaurants didn't. Hospitality lost 3.83% of transactions year-on-year in H1; Nightlife lost 3.95%. Travel grew 0.97% in Q1, with Entertainment & Leisure up 6.16%.

Inflation is doing the heavy lifting on the high street. Hospitality, Nightlife, and Everyday Conveniences all posted positive spend growth — but only because average ticket value rose around 5%. Real visit frequency is falling.

Retail is winning volume and losing value. Non-Essential Retail transactions rose 6.09% in H1 while average basket size fell 4.15%. Consumers are shopping more often and spending less per basket — a clear discount-led signal.

Spend and transactions tell two different stores

Unlock the full Q2 State of Spend report

Top-line growth is masking a structural pullback in mid-week dining, a narrowing active customer base, and a discount-driven retail shift. Download the full report for the category-by-category breakdown and the four advertiser playbooks for an uneven wallet.

Inside the report:

- The "Who Is Losing?" Index: How six macro categories really performed once ATV inflation is stripped out.

- The Hospitality & Nightlife Squeeze: Why footfall is down ~4% even as spend ticks up.

- The Retail Paradox: Record transaction frequency colliding with shrinking baskets.

Four Playbooks for Advertisers: Where to drive frequency, where to grow basket size, and where loyalty beats acquisition in Q3.

Cardlytics Banking Loyalty Index 2026

From loyalty to relevance: Why personalised rewards matter more than ever for UK banks

UK consumers may feel loyal to their bank, but that loyalty is increasingly conditional.

New research from Cardlytics, based on a nationally representative survey of 4,000 UK adults, shows that while most customers are not actively planning to switch, many are open to reassessing where they bank when the value is clear.

Two thirds of consumers (65%) say they feel loyal to their main bank, and 60% say they are unlikely to switch in the next 12 months. But that stability should not be mistaken for permanence. More than half (57%) have switched their main bank account at some point as an adult, and many now spread their money across more than one provider.

The result is a banking market where retention is no longer just about keeping customers from leaving altogether. It is about staying relevant in more of their everyday financial decisions.

Trust and service still matter, but they are now the baseline

When asked what keeps them with their current bank, UK consumers are most likely to cite good customer service (40%), brand trust and reputation (35%), and the quality of mobile or online banking (32%).

These are the foundations of a strong banking relationship. They help explain why customers stay put, particularly older generations. For example, Baby Boomers are significantly more likely to say customer service is a key reason they stay with their bank (50%).

But these factors are increasingly expected. They are essential to retention, but on their own they may be less effective at creating real competitive advantage.

Unlock the full Cardlytics Banking Index 2026

The shift from passive loyalty to active relevance is changing how the UK banks. To read the full analysis on how financial value triggers action, the impact of personalised rewards on 18 to 34 year olds, and why loyalty is no longer exclusive, download the complete report below.

Get the full insights to discover:

- The Switching Triggers: The specific financial incentives driving 25% of Gen Z to reconsider their bank.

- The Personalisation Opportunity: How tailored rewards can increase retention by up to 55% for key demographics.

- The Visibility Challenge: Why 22% of customers are unaware of the rewards their banks already offer.

- Multi-banking Trends: Why customers are spreading their finances and how to capture a greater share of wallet.

Where have all the shoppers gone?

Where have all the shoppers gone?

How UK shoppers are narrowing their choices — and what it means for growth

After two years of post-pandemic recalibration, UK consumers are still spending. But they are becoming more selective in where, when and why they do so.

Cardlytics’ latest State of Spend report draws on first-party purchase data from 23 million UK bank customers across the spring and summer period.

What it shows is simple: retail growth remains present, but increasingly uneven. Categories that feel essential, convenient or low-risk continue to attract spend. More discretionary and deferrable purchases are coming under greater pressure.

This is less a story of demand disappearing and more one of decision-making narrowing. For retailers and brands, growth will depend less on broad consumer momentum and more on securing a place in a smaller set of deliberate purchasing moments.

Essentials: fewer trips, tighter control

Essential categories remain the most resilient part of the market. But the pattern of spending suggests households are becoming more deliberate in how they manage everyday needs. Growth is still there — it is just concentrated in channels that offer either convenience at scale or a clearer sense of value.

The strongest performance continues to come from Digital & Delivery Grocery, where spend rose 17% in 2024 and 14% in 2025. Transactions also grew strongly, pointing to a channel still benefiting from continued adoption and slightly larger baskets.

Discounter Grocery shows a similar pattern, with spend up 9% in 2024 and 7% in 2025, supported by steady transaction growth. The category continues to act as a dependable value channel for households managing budgets carefully.

Among Big Grocers, growth is more subdued — 6% in 2024, slowing to 3% in 2025 — while transactions moved broadly flat. Spending is being held up by larger baskets rather than more visits. Convenience Grocery has come under greater pressure still, with trips down around 3%.

Fuel is the clearest sign of retrenchment within essentials. Spend declined 5% in 2024 and 10% in 2025, with early 2026 data indicating this behaviour is continuing.

Cardlytics analysis

Essential spend is still being protected, but the shape of that spend is changing. Consumers are concentrating everyday purchasing into channels that help them feel organised or in control — whether that’s delivery-led convenience or discounter-led value.

For marketers, the opportunity is less about generating additional need and more about intercepting planned purchase moments with a clear reason to choose one retailer or brand over another. In a market where fewer shopping occasions carry more weight, securing a greater share of each visit matters more.

Retail: a resilient base, but narrowing engagement

Retail continues to grow — but that growth is becoming more uneven. The strongest performance is increasingly concentrated in categories that feel accessible, repeatable or easy to justify. Traditional and aspirational areas are finding it harder to sustain engagement.

Make-up & Beauty remains one of the clearest areas of resilience. Spend rose 11% in 2024 and 8% in 2025, with transactions also moving in the right direction. It’s one of the few categories where shoppers still see room for smaller, more manageable discretionary purchases.

Online Fast Fashion continues to expand, up 14% and 9% across the two years, though baskets have softened slightly — shoppers engaging more frequently but with tighter control on basket size. Marketplaces are another strong area of growth, reinforcing their role as a flexible, value-conscious route to purchase.

Elsewhere, the picture tightens. High Street Fashion growth has slowed and transactions have flattened. Department Stores saw spend fall 3% in 2024 and 4% in 2025, pointing to an ongoing footfall challenge. And Luxury / Designer Fashion spend declined 6% in 2024 and 8% in 2025 — purchases are still happening, but among fewer shoppers, less often.

Cardlytics analysis

The categories still growing are not necessarily those with the strongest brand pull. They are the ones most aligned with how consumers want to shop now: flexibly, frequently and with lower perceived risk.

For brands, that raises the importance of relevance, value communication and mission-based targeting over broader assumptions about seasonal demand. In a more selective market, success will depend less on broad visibility alone and more on giving shoppers a clear, immediate reason to engage.

Household: from upgrade to upkeep

Across home-related categories, the shift from 2024 into 2025 points to a more cautious consumer mindset. Spending hasn’t disappeared — but households are more willing to maintain and replace than to embark on larger, more discretionary home purchases.

Value Homeware has remained relatively stable, up 9% in 2024 and 5% in 2025. High Street Furniture shows a clearer slowdown, moving from 6% growth to 2%, with spend concentrating in fewer, higher-value occasions.

The pattern is more pressured in DIY. After 3% growth in 2024, spend moved into a 2% decline in 2025, with transactions down around 5%. Electricals follow a similar trajectory — from 4% growth to a 1% decline — with purchases increasingly concentrated in fewer, more considered buying moments.

Cardlytics analysis

In home-related categories, demand increasingly looks tied to maintenance, replacement and justified necessity rather than inspiration or upgrade. That changes what effective messaging looks like.

Brands here may need to focus less on aspiration and more on practicality, durability and timely relevance if they want to convert consumers who are clearly weighing whether a purchase can wait. The strongest opportunities come from moments where need is immediate and the value exchange is clear.

Wider discretionary: where the drop-off is most visible

The clearest signs of pressure appear outside the core retail categories — in areas where spending is most optional and easiest to postpone. Here the challenge is not how much consumers spend when they engage, but whether they enter the category at all.

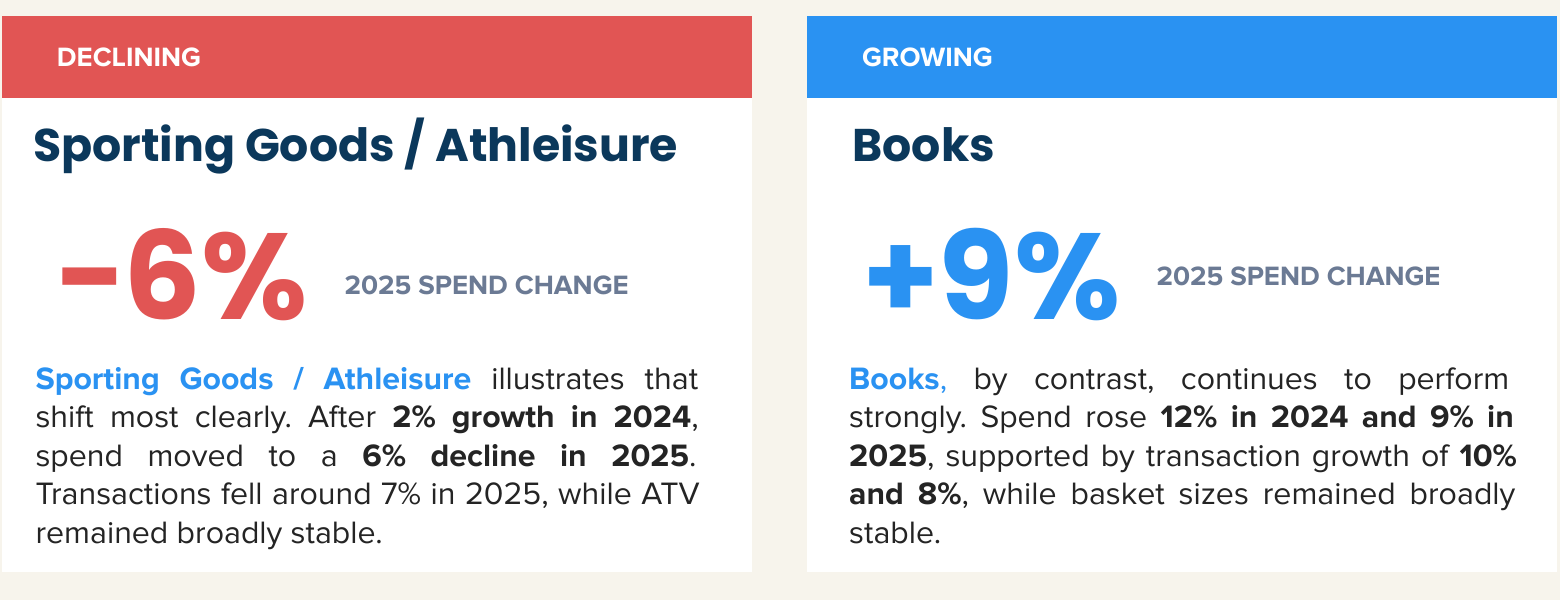

Sporting Goods / Athleisure illustrates the shift most clearly. After 2% growth in 2024, spend moved to a 6% decline in 2025, with transactions down around 7% while ATV stayed broadly stable. The pressure is being driven by fewer shoppers choosing to participate — not by smaller baskets.

Books, by contrast, continues to perform strongly, up 12% in 2024 and 9% in 2025. It remains one of the clearest examples of a discretionary category where engagement holds up — consumers are still willing to spend where purchases feel lower-cost, familiar or easy to justify.

The issue is no longer simply whether shoppers can spend, but which categories still make the cut.

Cardlytics analysis

For discretionary categories, the core challenge is re-engagement. When consumers are reducing the number of optional purchases they make, brands need stronger triggers to prompt participation in the first place.

That may mean leaning harder into immediacy, occasion-based relevance, perceived value or more functional reasons to buy — rather than assuming promotions alone will unlock demand. Growth depends less on broad category momentum and more on giving consumers a compelling reason to opt in at all.

Looking ahead into 2026

Early 2026 performance is already pointing to where the narrowing of shopper demand is concentrating. Online pharmacy revenue is driving Beauty category growth. Health & wellbeing FMCG is up against overall category decline. Electronics AOV is rising on accessories, PC and gaming. And Paint & Home Furnishings are rising even as DIY declines — a clear signal that the channel and use-case shifts identified in this report are continuing.

Fewer decisions, higher stakes

The summer shopper has not disappeared, but the number of decisions they appear willing to make has narrowed.

Across the market, the strongest performance is coming from categories that feel essential, convenient or easy to justify, while more deferrable and aspirational purchases are facing greater pressure. That does not point to a collapse in consumer demand — it points to a consumer mindset that is becoming more selective about where spending feels worthwhile.

For retailers and brands, that creates a more competitive environment. Growth is no longer just about being present at the point of purchase — it is about being relevant enough to be included in a smaller set of deliberate decisions. In that context, value, timing and clarity matter more, particularly in categories where engagement can no longer be taken for granted.

How marketers should show up

01. Protect existing shoppers first

Shoppers don’t leave in one move — they drift. Transaction data already shows who’s slipping. Reaching a lapsed shopper around their next likely need window is cheaper than finding a replacement, and more effective than broad re-acquisition.

02. Growth sits in small, repeat purchases

The categories still expanding are the ones where the purchase feels small, familiar and easy to justify. Find the version of your product that fits a smaller, more frequent moment — something a shopper says yes to without deliberation.

03. Solve for participation, not basket size

The harder question isn’t what a shopper spends when they show up — it’s whether they show up at all. Discounting rarely pulls someone into a category they’ve stepped out of. An immediate, tangible need does.

The brands best placed to outperform will be those that understand which purchase moments consumers still prioritise — and can show up in those moments with a clear and compelling reason to buy.

Talk to Cardlytics about how purchase intelligence and card-linked offers can help your brand secure a place in a smaller, more deliberate set of consumer decisions — www.cardlytics.com

Q1 2026 State of Spend: The controlled consumer

The Controlled Consumer:

Why UK shoppers entered 2026 already spending with intent

The New Year value hunt started before Christmas.

Cardlytics’ State of Spend analysis of Q4 2025 and early Q1 2026 shows that UK consumers did not loosen their spending habits over the festive period. Instead, they became more deliberate about how and where they spent. Drawing on card-based transaction data from over 23 million bank accounts, the analysis points to a shift toward a more controlled approach to spending that is now shaping behaviour into 2026.

The last State of Spend showed that UK consumers had returned to the market, but with conditions. Spending resumed, but cautiously. Shoppers scrutinised price, convenience and perceived quality, pulling back when expectations were not met. Consumers would still spend, but largely when prompted by the right offer or moment.

The latest data shows that this scrutiny has since become embedded in shoppers’ habits. December revealed how consumers were already operating under tighter decision-making rules as they approached the new year.

With inflation ticking up again at the end of the year, cost pressures remained firmly in place. Rather than retreating from spending altogether, consumers adapted — switching formats, trading down and filtering purchases more aggressively. Festive spending held, but it was more controlled, with loyalty weakening and defaults increasingly questioned. As a result, consumers entered Q1 already spending more selectively.

Read the full report by downloading it here.

The Golden Quarter is Changing: Inside the 2025 State of Spend

The Golden Quarter is Changing: Inside the 2025 State of Spend

The UK’s peak retail season is evolving. Consumers are still spending, but they’re more selective, strategic, and values-driven than ever before. Based on spend data from over 23 million UK bank accounts and nationally representative research, Cardlytics' State of Spend report uncovers what’s shaping the 2025 Golden Quarter — and where brands should focus to win.

Headline Trend Summaries (With Light Stats)

1. Black Friday is no longer the main event

The era of single-day shopping spikes is fading. Our data reveals that consumers are spreading spend across weekends and early December instead. Brands focused only on the Friday are missing the bigger picture.

2. Gifts that matter and don’t just impress

Over half of consumers say they’re choosing meaningful or practical gifts this year. Beauty and books are holding strong, while luxury and electrical categories are losing ground.

3. Fashion is fragmenting

Fast fashion still performs, but growth is slowing. Shoppers are shifting toward resale platforms and marketplaces that offer affordability and sustainability in one.

4. Grocery is about confidence, not just cost

Spend is still rising across grocery - but discounters, delivery services, and high-end grocers are outpacing traditional supermarkets. Value is no longer just about price; it’s about trust and convenience.

Consumers are still buying. They’re just doing it on their terms. The winners in 2025 will meet them where they are — with relevance, value, and visibility.”

Want the full data?

The full report includes:

- Category-by-category breakdowns from 2022 to 2024

- 2025 retail forecasts across 14 key sectors

- Consumer behaviour insights and shopping intent

- Strategic recommendations for campaign planning

Download the Full Report

UK Loyalty Movement Report: Retail

UK Loyalty Movement Report: Retail

Introduction

In our previous report, Redefining Customer Loyalty, Cardlytics defined loyalty as a consumer’s preference for a merchant over its competitors, analysing spending across six industries to measure customer loyalty and spending patterns with both loyal and non-loyal customers.

But customer behavior isn’t fixed - customers shift between loyalty segments over time. Understanding these shifts helps identify churn and informs strategies to nurture relationships and move customers to higher loyalty segments. In our UK Loyalty Movement Report, we dive into customer behavior in the Retail category to better understand engagement over time by analyzing more than £245 billion in consumer spend behavior.*

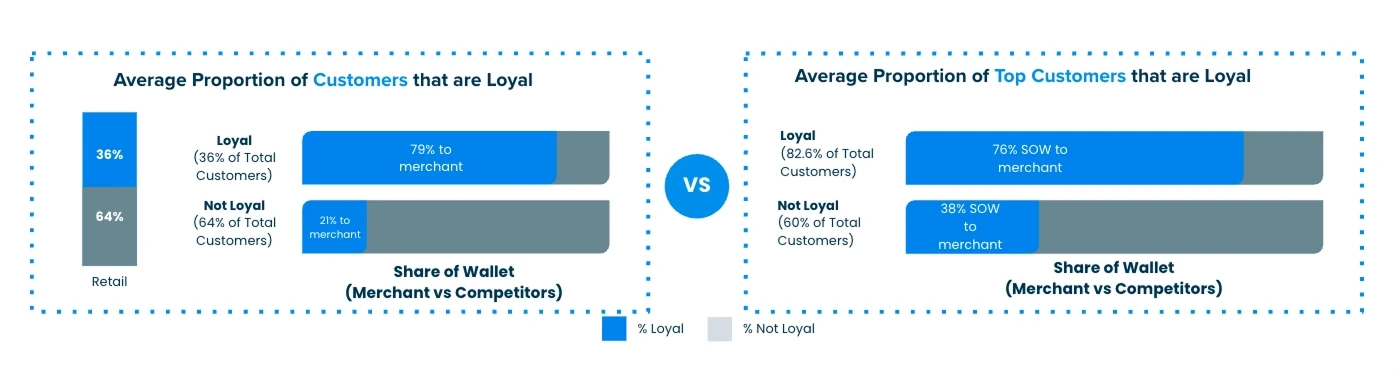

Retail Category Loyal Customers

On average, 64% of a merchant’s customers are not actually loyal. But the loyal segment has a much higher share of wallet (79%) than a not loyal segment (21%).

Top Customers (top 20% of most frequent transactors) show a strong uptick as loyal vs not loyal customers. But the loyal customer segment shows more than 3x higher share of wallet.

Findings

We looked into purchase data across Retail in the UK over the last 8 quarters (Q1-23 through Q4-24) on a quarter by quarter basis to see whether even the “most loyal” customers showed changes in their purchase behavior.

Retail Loyalty Movement

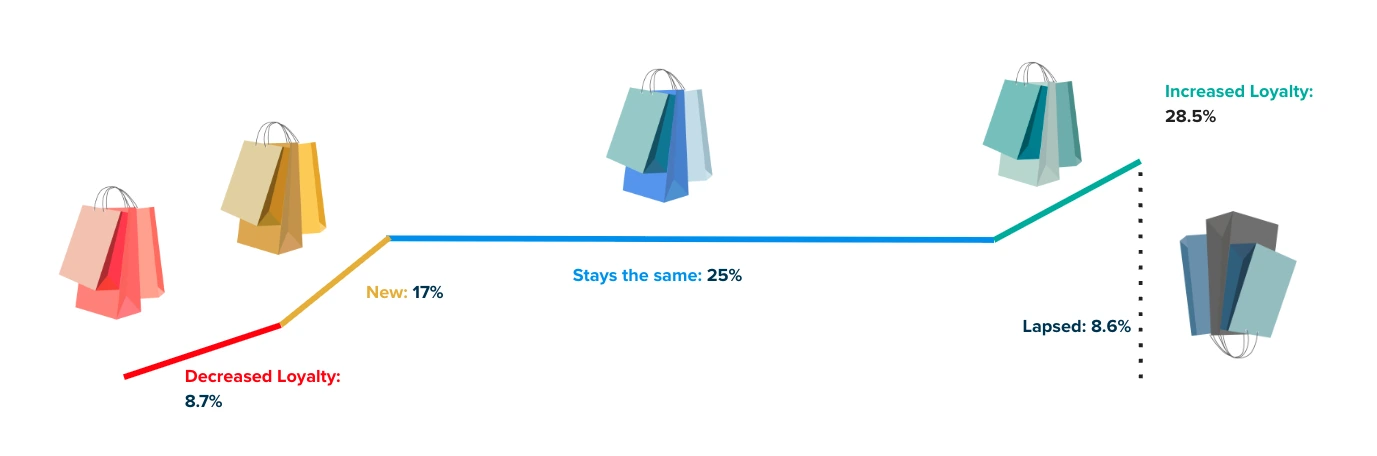

Overall, quarter over quarter, 25% of customers tend to remain in their existing segments while 37.2% increase or decrease their loyalty to a merchant. Yet there is much more extensive customer loyalty movement within the “not loyal” segments.

Segment movement

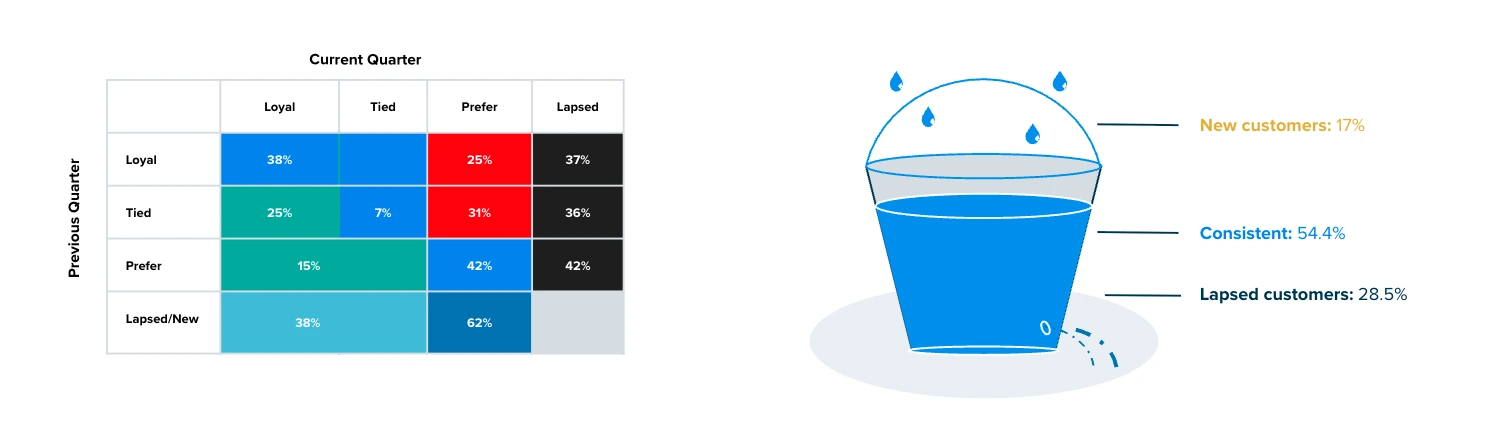

The Tied segment (part of the Not Loyal group) demonstrates the most volatility — with just 7% remaining stable and 29% moving up and 29% moving down into other segments.

Retail Leaky Bucket

Retail brands are acquiring new customers yet even more existing customers are moving into the lapsed tier. This cycle can be reversed by continuing to nurture existing customers.

Diving deeper into the individual segments tells us:

- Loyal customers and those that Prefer the competition are the most stable segments, with 38% and 42% respectively staying in the same category from one

quarter to the next. This indicates a strong commitment to brand preference — whether for your brand or a competitor's. - Customers in the Tied segment exhibit the highest level of movement, with just 7% remaining Tied quarter-over-quarter. These shoppers are the most susceptible to influence and represent a key opportunity for brands aiming to tip the scales in their favour.

- Interestingly, Loyal customers still show a 25% lapsed rate, which is comparable to the Tied segment’s 36% lapsed rate. This suggests that attrition among Loyal customers may not be driven by brand disengagement, but rather by natural gaps in purchase cycles — for example, customers who buy apparel less frequently.

Definitions of Customer Segments

Loyal Customers:

- Loyal: Only shop with a specific brand, or have the highest share of wallet with a given brand and relative rank is lower than all other brands in consideration set

Not Loyal Customers:

- Tied: Similar relative ranks to 2 or more brands regardless of share of wallet ranking

- Prefer: Lower share of wallet and higher rank than other brands in their consideration set

- Lapsed: Shopped historically but do not shop currently, as defined by the analysis time period

- New: Shop currently but have not shopped historically, as defined by the analysis time period

Takeaways

Marketers know it’s more costly to acquire or re-acquire customers than to keep existing ones engaged. When brands neglect current customers, they risk losing them and undoing past investment yet the reasons why a customer might “lapse” is different depending upon their loyalty tier. Loyalty is fragile and demands ongoing effort as competition is always close by. To stay top of mind, marketers must continuously nurture relationships, understand customer needs, and offer seamless experiences. To foster loyalty with your customers, consider these recommendations:

- Use an “always on” strategy to keep customers engaged, regardless of purchase

frequency. - Regularly update/refine customer segments and adjust reward offers to keep

them engaged. - Use targeted campaigns to boost loyalty and revenue.

Cardlytics can deliver a comprehensive Customer Loyalty Analysis with insights into customer behavior and movement across defined loyalty segments. Contact us for more details.

* For this report, we've selected the entire retail category in our data, collectively representing over £245bn in annual card spend. This sample differs from the previous Customer Loyalty Analysis report.

UK State of Spend Report: Retail

"If the price is right"

New Cardlytics State of Spend study reveals tentative recovery in consumer confidence

After two years of post-pandemic recalibration, UK consumers are shopping again – just not like they used to.

The latest data from Cardlytics reveals a retail landscape defined less by indiscriminate demand and more by considered choice.

While spending remains resilient in many categories, shoppers are now clearly applying more scrutiny to how and where they spend. Value, convenience, and perceived quality are under the microscope, and if expectations aren’t met, consumers are pulling back.

This divergence is playing out differently across the retail sector. Categories like high-street fashion and beauty are holding strong, buoyed by brand loyalty, reviving high streets, and the occasional feel-good purchase.

But grocery and household tell a more precarious story, where price sensitivity and shifting shopping habits are forcing brands to work harder and smarter to keep customers loyal.

Whether shopping in-store, online, or through delivery apps, today’s consumer expects more than just competitive pricing.

They’re looking for value that feels personal. For retailers, the challenge is clear: speak directly to customer priorities, or risk being left behind.

Retail: A resilient core – but rewards go to relevance

Fashion and beauty continue to defy broader economic headwinds. Spending on make-up and beauty products surged by 19% year-on-year in Q1 2024, and growth has carried into 2025, albeit at a more modest 5%. The number of transactions in the sector has outpaced spend, suggesting that while shoppers remain engaged, they are consciously managing budgets – opting for smaller, more frequent purchases that still offer a sense of indulgence. It’s a pattern that reflects the so-called “lipstick effect”: the tendency for consumers to turn to affordable luxuries during uncertain times.

High street fashion is also faring well. After growing 9% in 2024, the category recorded a further 5% uptick in early 2025, driven by established brands with a strong physical presence and a loyal customer base. This comes despite recent cyber attacks on major retailers, which - in good news for the sector - hasn’t deterred shoppers as of yet. Rather than stop spending, it just shifted it - as shoppers showed they are loyal to their habits over individual brands.

Online fast fashion, meanwhile, showed little momentum through 2024, but increased sharply in Q1 2025 with a 13% rise in spend. Discount-led promotions and trend-led buying may be drawing cautious consumers back to basket - but this trend remains nascent stages.

However, not all categories are experiencing this trend. Department stores saw a 4% drop in spend in 2024, with a further 5% decline in 2025. Transactions have followed the same downward trajectory, pointing to a broader shift away from traditional department store formats. As shoppers prioritise experience, value and, crucially, brand alignment, department stores may be losing relevance to more focused propositions.

Cardlytics Analysis

Retailers that combine physical presence with a strong sense of brand identity continue to perform strongly. But brands can no longer rely on habitual customer loyalty. Our data shows clear momentum for brands that are giving customers a feel-good factor to shopping, whether that be through price, experience or personalisation.

Case Studies

- A leading e-commerce & retail brand partnered with CDLX to drive new customers and ensure incremental revenue, by leveraging CDLX’s pay-per-performance channel to incentivise spend from competitors via cash back reward. The campaign delivered £1m revenue across 20K redemptions, captured 27% SoW across redeemers from competitors. Across the “New” segment, CDLX captured 77% SoW from competitors.

- A major European health & wellness brand partnered with CDLX to acquire new customers, re-engage and retain lapsed and existing customers, and drive sales over a six week period in Q1 2025. Leveraging our proprietary transaction data into data-driven marketing, the campaigns drove over £2M Revenue and an average ROAS of £24.41. During that period, the brand increased share of wallet by 52%, crucially gaining ground on key competitors in the health and wellness industry.

Grocery: Essential, but under pressure

Supermarkets remain a staple of consumer spending, but the data tells a story of growing caution. After recording 9% growth in 2024, so-called ‘big grocers’ saw a 3% fall in spend in the first quarter of 2025. The number of transactions have held steady however, suggesting that shoppers are still showing up – they’re just spending less when they do.

This theme appeared prominently across convenience grocery.

Spend rose by 11% in 2024, before dipping 4% this year. Unlike the supermarkets, however, transaction volumes declined modestly, pointing to a broader behavioural shift. Shoppers appear to be planning more carefully, opting for fewer top-up trips and returning to larger, weekly shops.

In contrast, grocery delivery continued to grow, extending its gains from last year. After a 16% rise in 2024, the category saw a further 13% increase in early 2025, with both the average transaction value and number of orders increasing. Once considered a pandemic-era habit, online grocery ordering now looks like a lasting behavioural shift – particularly for customers who value predictability, convenience and the ability to budget in advance.

Cardlytics Analysis

The return of the big weekly shop, combined with the decline in spontaneous convenience visits, signals a shift towards planned, value-driven behaviour. For grocers, this is both a challenge and an opportunity.

The ability to personalise offers, reinforce loyalty, and remove friction at checkout is becoming critical, particularly as shoppers become more deliberate in how and where they spend. Cashback rewards can help bridge the gap between price expectations and perceived value, especially when tailored to individual behaviours. Delivery providers are responding well to this shift, offering consistent, low-surprise experiences that support budgeting and convenience. A similar customer-first approach is increasingly expected in-store, where value and planning now take precedence over impulse.

Case Study

A leading food delivery platform and CDLX partnered to drive new customer acquisition and incremental revenue, using cashback rewards to incentivise spend from competitors.

The campaigns delivered 119K redemptions and £2.9M in revenue, capturing 44% share of wallet across lapsed and acquisition segments. Incremental revenue from the "New" customer segment alone reached £470K, with repeat customers generating an additional £7.2M in spend post-campaign.

Household: Still spending, but pulling back

After a period of steady post-pandemic investment in the home, household spending is beginning to cool. While consumers are still investing in their living spaces, they are doing so with increasing caution – prioritising essential upgrades over discretionary improvements. Across all categories, the number of transactions has remained broadly stable, but average spend is softening – indicating a shift towards smaller, more deliberate purchases.

This was the case for DIY, which saw spend increase modestly by 4% in 2024, before falling 1% in early 2025. Transaction volumes held steady, but average spend edged down – showing that consumers are now focusing on smaller-scale fixes or improvements, rather than large projects.

Value homeware followed a similar pattern, emphasising the importance of affordability in the household goods sector. While total spend softened, the number of transactions held firm, showing a consumer preference for incremental upgrades that deliver a sense of progress without straining budgets. Elsewhere, spending on garden and outdoor products declined in early 2025, reflecting a clear pivot towards core priorities, with seasonal or aspirational purchases falling by the wayside.

Spend for electricals declined by 6% in 2025, alongside a 7% fall in transactions. But average spend rose 6%, suggesting a more selective, quality-focused approach to purchasing habits. Consumers appear to be waiting longer between purchases, but when they do buy, they are choosing higher-spec replacements – reinforcing the idea that perceived value, rather than just price, is driving decision-making.

Cardlytics Analysis

In the household sector, the rules of engagement have changed. Big-ticket spending is cooling, but our data shows that consumers are still willing to invest when they feel the value is tangible, especially on higher-spec replacements in categories like electricals.

Cashback rewards are proving particularly effective in this space, encouraging considered purchases while reinforcing the idea of getting more for less. Retailers focused on affordability are outperforming their lifestyle-led counterparts.

The signal from consumers is clear: value and functionality matter more than non-essential or lifestyle-led propositions. Brands that demonstrate they understand their customers’ priorities - and reinforce that through personalised offers and targeted cashback - will go further in earning loyalty and driving conversion.

Case Study

A leading DIY brand and CDLX partnered to improve incremental sales, drive new customers and repeat visits as well as deepen loyalty with existing customers. Using CDLX’s proprietary purchase intelligence data, the campaigns identified and targeted customers with personalised value-driven offers.

Over the six-week period, over £800k in incremental sales were driven. The brand has seen 39% of campaign customers return to shop again, and captured 60% share of wallet from key competitors during that time.

Navigating a more cautious consumer landscape

Our analysis for the first four months of 2025 painted a clear picture of an increasingly value-conscious consumer. While there were bright spots — such as sustained demand for affordable luxuries and resilient online grocery growth — the broader retail environment showed signs of growing caution. The data indicated that a softening in consumer confidence could be on the horizon — something that recent retail sales figures from May have now confirmed, with sharp drops in sales linked to rising inflation and consumer cutbacks.

The opportunity for brands lies in how they respond. Our data shows that personalisation, value-driven propositions, and transparent rewards are more important than ever. Shoppers are still spending, but they are making deliberate choices about where they see true value. Cashback rewards and tailored offers can play a crucial role in reinforcing loyalty and driving conversion during this period of increased scrutiny.

For retailers, the message is clear: relevance, value, and trust must be at the heart of every interaction. Businesses that consistently prove they can deliver meaningful value at the right price will be best positioned to secure customer loyalty and drive sustainable growth in the uncertain months ahead.

UK Loyalty Movement Report: Airline

Airlines: Unpacking the State of Customer Loyalty

Introduction

Previously, Cardlytics defined loyalty as a consumer’s preference for a merchant over its competitors.* We analyzed billions in spending across six industries to measure customer loyalty and spending patterns with both loyal and non-loyal customers.

But customer behavior isn’t fixed—customers shift between loyalty segments over time. Understanding these shifts helps identify churn and informs strategies to nurture relationships and move customers to higher loyalty segments. In our Loyalty Movement Report, we dive into the Airline category to better understand engagement over time by analyzing more than £40B in consumer spend behavior.

.png)

Findings:

We looked into purchase data at all Airlines in the UK over the last 8 quarters (Q1-23 through Q4-24) on a quarter by quarter basis to see whether even the “most loyal” customers showed changes in their purchase behavior.

Segment Movement

.png)

Of the portion of each customer segment that is non-lapsed, those that are loyal to a specific airline show the strongest brand retention - 31% remain loyal quarter over quarter. In contrast, Tied and Prefer customers demonstrate greater variability in behaviour, with only 4% and 12% respectively maintaining their previous preference.

Loyal customers tend to remain consistent in their airline choice, likely driven by the strength of airline loyalty programmes and exclusive incentives. However, Tied and Prefer customers show clear signs of behaviour fluidity, highlighting a key opportunity for targeted campaigns to drive conversion toward brand loyalty.

Lapsed behaviour is high across all segments—65% of previously loyal customers lapsed, and similar rates are observed among Tied (63%) and Prefer (67%) segments. This reflects typical airline purchasing patterns, where customer loyalty can be disrupted by pricing, availability, or external factors, regardless of prior loyalty classification.

Airlines Leaky Bucket

Airlines are acquiring new customers yet even more existing customers are moving into the lapsed tier. This cycle is expected based on typical consumer behavior for airline travel quarter over quarter but reinforces need to nurture existing relationships.

.png)

Takeaways:

Airline marketers’ inherent focus on nurturing loyal customers is well-know and consumer spend data show it’s working - Loyal customers tend to stay loyal. But huge opportunity exists with customers who are not loyal to any specific airline and could be lured through greater incentives. To stay top of mind, marketers must continuously nurture relationships, understand customer needs, and offer seamless experiences. To foster loyalty with your customers, consider these recommendations:

- Use an “always on” strategy to keep customers engaged, regardless of purchase frequency.

- Regularly update/refine customer segments and adjust reward offers to keep them engaged.

- Use targeted campaigns to boost loyalty and revenue.

Cardlytics can deliver a comprehensive Customer Loyalty Analysis with insights into customer behavior and movement across defined loyalty segments. Contact us for more details.

Loyalty Movement Report: Apparel

Apparel: Stop Taking Customer Loyalty for Granted

Introduction

In our previous report, Redefining Customer Loyalty, Cardlytics defined loyalty as a consumer’s preference for a merchant over its competitors. We analyzed $160B in spending across six industries to measure customer loyalty and spending patterns with both loyal and non-loyal customers.

But customer behavior isn’t fixed—customers shift between loyalty segments over time. Understanding these shifts helps identify churn and informs strategies to nurture relationships and move customers to higher loyalty segments. In our Loyalty Movement Report, we dive into customer behavior in the Apparel category to better understand engagement over time by analyzing more than $17B in consumer spend behavior.*

Apparel Category Loyal Customers

On average, 61% of a merchant’s customers are not actually loyal. But the loyal segment has a much higher share of wallet (85%) than a not loyal segment (21%).

.png)

Top Customers (top 10% of most frequent transactors) show a +6 point uptick as loyal vs not loyal customers. But the loyal customer segment shows more than 3x higher share of wallet.

Findings

We looked into purchase data at all Apparel brands in the US over the last 8 quarters (Q1-23 through Q4-24) on a quarter by quarter basis to see whether even the “most loyal” customers showed changes in their purchase behavior.

Apparel Loyalty Movement

Overall, quarter over quarter, 41% of customers tend to remain in their existing segments while 16% increase or decrease their loyalty to a merchant. Yet there is much more extensive customer loyalty movement within the “not loyal” segments.

.png)

Segment Movement

While all segments show purchase behavior movement, the Tied segment (part of Not Loyal customers) shows the most movement - both up (29%) and down (29%) - into other segments.

.png)

Apparel Leaky Bucket

Apparel brands are acquiring new customers yet even more existing customers are moving into the lapsed tier. This cycle can be reversed by continuing to nurture existing customers.

.png)

Diving deeper into the individual segments tells us:

- Loyal customers and those that Prefer the competition are the most rigid (with 57% and 58% staying the same, respectively). Those customers that are Tied have the greatest propensity for a behavior change (with only 18% staying the same).

- While the most Loyal customers show a 25% lapsed rate at similar levels as Tied, this is most likely not connected to churn vs connected to cadence of shopping behavior (maybe they don’t buy clothes every that frequently).

Definitions of Customer Segments

Loyal Customers

Loyal: Only shop with a specific brand, or have the highest share of wallet with a given brand and relative rank is lower than all other brands in consideration set

Not Loyal Customers

Tied: Similar relative ranks to 2 or more brands regardless of share of wallet ranking

Prefer: Lower share of wallet and higher rank than other brands in their consideration set

Lapsed: Shopped historically but do not shop currently, as defined by the analysis time period

New: Shop currently but have not shopped historically, as defined by the analysis time period

Takeaways

Marketers know it’s more costly to acquire or re-acquire customers than to keep existing ones engaged. When brands neglect current customers, they risk losing them and undoing past investment yet the reasons why a customer might “lapse” is different depending upon their loyalty tier. Loyalty is fragile and demands ongoing effort as competition is always close by. To stay top of mind, marketers must continuously nurture relationships, understand customer needs, and offer seamless experiences. To foster loyalty with your customers, consider these recommendations:

- Use an “always on” strategy to keep customers engaged, regardless of purchase frequency.

- Regularly update/refine customer segments and adjust reward offers to keep them engaged.

- Use targeted campaigns to boost loyalty and revenue.

Cardlytics can deliver a comprehensive Customer Loyalty Analysis with insights into customer behavior and movement across defined loyalty segments. Contact us for more details.

* For this report, we've selected the entire Apparel category in our data, collectively representing $17bn in annual card spend. This sample differs from the previous Customer Loyalty Analysis report.

About Cardlytics

Cardlytics (NASDAQ: CDLX) is a commerce media platform, powered by our publishers’ first-party purchase data, that makes commerce smarter and more rewarding for everyone. We offer a range of solutions to help advertisers and publishers, including financial institutions, grow and strengthen customer loyalty. With visibility into approximately half of all card-based transactions in the U.S. and a quarter in the U.K., Cardlytics enables advertisers to engage consumers at scale and drive incremental sales through our industry-leading financial media network. Publisher partners can enhance their platforms with relevant and personalized offers that improve the shopping experience for their customers. Cardlytics also offers identity resolution capabilities through Bridg, which helps convert anonymous shoppers into known and reachable customers. Headquartered in Atlanta, Cardlytics has offices in Menlo Park, Los Angeles, Champaign, New York and London. Learn more at www.cardlytics.com or follow us on LinkedIn.

Get our insights delivered to you

Stay up to date. Subscribe now.